How Build Stage Payments Work for Off-Plan New Builds

Published by New-Builds Team · 2025

Buying a new build home off-plan — that is, purchasing a property before it has been constructed or while it is still under construction — is one of the most popular routes into new build homeownership in the UK. Major developers like Barratt Homes, Taylor Wimpey, Persimmon, Bellway, and Redrow all offer off-plan purchasing options, and for good reason: it allows buyers to secure a property at today's price, choose their preferred plot, and often customise finishes and layouts before the home is built. However, the financial mechanics of an off-plan purchase differ significantly from buying a completed property, and understanding how build stage payments work is essential for any buyer considering this route.

Unlike purchasing an existing property where the entire purchase price is transferred on completion in a single transaction, off-plan new builds can involve a more complex funding structure where mortgage funds may be released in stages as construction progresses. This stage payment process, governed by protocols established by the Council of Mortgage Lenders (CML, now UK Finance), involves inspections, certifications, solicitor involvement, and specific risk considerations that buyers need to understand before committing to a purchase. This guide explains the entire process in detail, from reservation through to final completion, ensuring you know exactly what to expect financially at every step. For guidance on choosing the right mortgage product for your off-plan purchase, see our comprehensive guide on how to effectively compare mortgage deals for new builds.

Understanding Off-Plan Purchases: The Basics

An off-plan purchase is any property transaction where you agree to buy a home that has not yet been completed. This can range from buying at a very early stage, where only the foundations have been laid (or in some cases, before any construction has started), through to buying a property that is nearing completion with just a few weeks of work remaining. The specific stage of construction at which you purchase affects the payment structure, the risks involved, and the financing options available to you.

Most UK new build buyers purchasing from major housebuilders will follow what is known as the "standard completion" model, where you pay a reservation fee, exchange contracts at some point during construction, and then pay the full purchase price on completion when the property is finished and ready for occupation. In this model, no mortgage funds are released until the property is complete, and the financial transaction closely resembles a standard property purchase, just with a longer gap between exchange and completion.

However, some off-plan purchases — particularly self-builds, custom builds, and certain smaller developer projects — use a stage payment structure where funds are released incrementally as the build progresses. This is where the CML stage payment framework becomes relevant, and understanding it is essential for managing your finances during the build period.

The CML Stage Payment Schedule

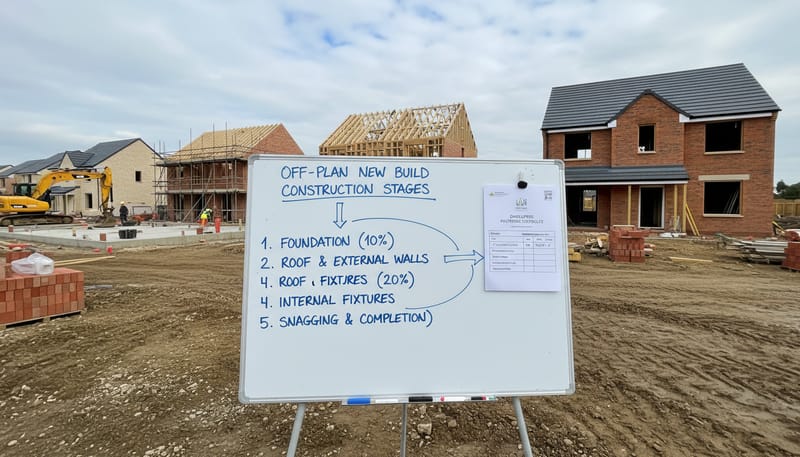

The Council of Mortgage Lenders (now part of UK Finance) established a framework for stage payments on new build properties that most lenders follow. This framework defines specific construction milestones at which mortgage funds can be released to the developer or builder. The standard CML stage payment schedule divides the build process into defined stages, each representing a significant construction milestone that is independently verified before funds are released.

The typical CML stage payment schedule for a standard new build house consists of six key stages, each triggering the release of a predetermined percentage of the total mortgage advance. The exact percentages can vary between lenders, but the industry-standard split is broadly consistent across the market. Understanding these stages helps you plan for the cash flow implications and understand what inspections and certifications are required at each point.

When and How Mortgage Funds Are Released

The process of releasing mortgage funds at each construction stage follows a strict protocol designed to protect both the buyer and the lender. Understanding this process helps you anticipate when funds will flow and what needs to happen before each stage payment is released.

At each stage, the following sequence of events occurs. First, the builder or developer notifies your solicitor (or conveyancer) that a particular construction stage has been reached. Second, the lender commissions an independent valuation or inspection to verify that the work has indeed been completed to the required standard. This inspection is carried out by a qualified surveyor or valuer who reports directly to the lender — not to the builder. Third, the surveyor provides a stage completion certificate confirming that the work meets the required standard and that the value of the partially completed property supports the funds being released. Fourth, the lender authorises the release of the stage payment to your solicitor, who then transfers the funds to the builder or developer.

The cost of these stage inspections varies between lenders but is typically £100 to £200 per inspection. With six standard stages, this adds £600 to £1,200 to your overall costs. Some lenders include one or more free inspections as part of their new build mortgage product, while others charge for every inspection. This is a cost that many off-plan buyers do not anticipate, so factor it into your budget from the outset. The inspections also take time — typically 5 to 10 working days from the stage being notified to the funds being released — which means there is always a short delay between the builder completing a stage and receiving payment.

The Solicitor's Role in Stage Payments

Your solicitor plays a central and critical role in the stage payment process, far more involved than in a standard property purchase. They act as the intermediary between you, the lender, and the builder, managing the flow of funds and ensuring that proper procedures are followed at every stage. Choosing a solicitor with specific experience of new build stage payment transactions is not just advisable — it is essential.

At each stage, your solicitor will receive the builder's notification that a stage has been reached, liaise with the lender to arrange the inspection, receive the surveyor's report and stage completion certificate, request the release of funds from the lender, and transfer the appropriate amount to the builder upon receiving the lender's authorisation. They also hold your deposit in their client account during the build period and ensure that appropriate protections are in place at each stage, such as verifying that the builder's warranty provider (NHBC, Premier Guarantee, LABC, etc.) has issued the appropriate interim cover.

The solicitor's fees for a stage payment transaction are typically higher than for a standard purchase because of the additional work involved at each stage. You can expect to pay 20% to 50% more in legal fees for a stage payment purchase compared with a standard completion. Some solicitors quote a fixed fee that includes all stages, while others charge a base fee plus an additional amount per stage. Clarify the fee structure before instructing your solicitor to avoid unexpected costs later.

Progress Inspections: What Surveyors Look For

The independent stage inspections commissioned by the lender are a critical safeguard in the stage payment process. These inspections verify that construction has genuinely reached the claimed stage, that the work has been carried out to an acceptable standard, and that the property's value at its current stage of construction supports the cumulative funds being released. Understanding what surveyors assess at each stage helps you understand the protections built into the system.

| Stage | Key Inspection Points | Typical Cost |

|---|---|---|

| Foundations | Depth, width, concrete quality, damp-proof course, drainage, ground conditions | £150–£200 |

| Wall Plate | Wall construction quality, mortar joints, cavity width, wall ties, lintels | £150–£200 |

| Roofed In | Roof structure, truss installation, tile/slate coverage, flashings, guttering | £150–£200 |

| Plastered | Plaster quality, first fix M&E compliance, insulation installation, internal layout | £150–£200 |

| Second Fix | Kitchen installation, bathroom suites, electrical testing, plumbing pressure tests | £150–£200 |

| Completion | Full property inspection, external works, energy performance, building regs sign-off | £150–£250 |

If a surveyor finds that work has not been completed satisfactorily or does not meet the required standard, they can withhold the stage completion certificate. This means the lender will not release the stage payment until the issues are rectified and a further inspection confirms compliance. While this can cause delays and frustration, it is ultimately a protection mechanism that ensures you are not paying for substandard work. As a buyer, you should welcome rigorous inspections rather than viewing them as an inconvenience.

Advance vs Arrears Stage Payments

There are two models for stage payments: advance and arrears. Understanding the difference is important because each carries different levels of risk and affects your cash flow differently during the build period.

Advance stage payments release funds before each stage of work begins. This means the builder receives money to fund the upcoming construction phase before the work is done. This model carries higher risk for the buyer because funds are released before the corresponding work is completed. If the builder encounters financial difficulties or ceases trading after receiving an advance payment, you have paid for work that has not been done. However, advance stage payments are sometimes necessary for smaller builders who need upfront funds to purchase materials and pay subcontractors. Self-build mortgages from lenders like BuildStore, Ecology Building Society, and Bath Building Society often use the advance payment model.

Arrears stage payments release funds after each stage of work is verified as complete. This is the safer model for buyers because you never pay for work that has not been done and independently inspected. The standard CML stage payment schedule described above operates on an arrears basis. Most mainstream lenders that offer stage payment mortgages use the arrears model, and it is the approach used for the vast majority of new build stage payment transactions in the UK. The builder funds each construction stage themselves and is reimbursed once the independent inspection confirms the stage is complete.

Interest Charges During the Build Period

A critical financial consideration that many off-plan buyers underestimate is the cost of interest during the build period. With stage payments, you begin paying interest on your mortgage from the date the first stage payment is released — not from the date you move in. This means you could be paying mortgage interest for several months while still living elsewhere and potentially paying rent, creating a dual-cost situation that requires careful budgeting.

The interest charges increase incrementally as each stage payment is released and the outstanding mortgage balance grows. After the first stage payment of 25%, you pay interest on that amount. After the second stage, you pay interest on 40% of the total advance. By the time the fifth stage is released (85% of funds), your interest charges are close to the full monthly payment amount. Only after the final 15% is released at completion are you paying interest on the full mortgage balance.

Over a typical 9 to 12 month build period, the cumulative interest paid before you even move in can total £5,000 to £8,000 or more, depending on the mortgage size and rate. This is money paid without any capital repayment benefit (during the build period, most stage payment mortgages operate on an interest-only basis), which is an additional cost of the off-plan purchase that needs to be factored into your overall affordability calculation.

Standard Completion vs Stage Payments: Which Will Apply to You?

If you are buying from a major UK housebuilder (Barratt, Taylor Wimpey, Persimmon, Bellway, Redrow, Berkeley Group, etc.), you will almost certainly follow the standard completion model rather than the stage payment model. This is because these developers have the financial resources to fund construction themselves and do not need buyers' funds during the build period. You will exchange contracts — typically paying a 5% to 10% deposit at this point — and then pay the remaining balance on completion when the property is handed over.

Stage payments are more commonly associated with self-builds (where you are building a home on your own land), custom builds (where you work with a builder to construct a bespoke home), smaller independent developers, and certain specialist developments. If you are purchasing from a developer who requires stage payments, it is essential to check that your mortgage lender offers a stage payment facility and that the stage schedule aligns with the developer's payment expectations.

The table below summarises the key differences between the two approaches to help you understand which model applies to your purchase.

| Feature | Standard Completion | Stage Payments |

|---|---|---|

| When funds released | All at completion | 6 stages during build |

| Interest charges start | Completion day | First stage release |

| Inspections needed | 1 (final valuation) | 6 (one per stage) |

| Lender availability | All lenders | Limited lenders |

| Typical use case | Major housebuilders | Self-build, custom build |

| Legal complexity | Standard | Higher |

Risks of Off-Plan Purchasing and How to Mitigate Them

Buying off-plan carries inherent risks that do not apply to purchasing a completed property. Understanding these risks and the protections available helps you make an informed decision and take appropriate precautions.

The most important protection against builder insolvency is the new home warranty. The NHBC Buildmark warranty, which covers approximately 80% of new build homes in the UK, includes pre-completion cover that protects your deposit (up to £100,000) if the builder fails to complete due to insolvency, fraud, or trading difficulties. This cover is in place from the date of registration (usually when your contract is exchanged) until the home is completed. Other warranty providers such as Premier Guarantee, LABC Warranty, and Checkmate also offer pre-completion protection, though the specific terms and coverage limits vary.

Mortgage Offer Validity: A Critical Factor

One of the most common practical problems with off-plan purchases is the mortgage offer expiring before the property is ready for completion. A standard mortgage offer is typically valid for six months, but many new build properties take longer than this to complete from the date the mortgage application is submitted. If the offer expires, you must reapply — potentially at higher rates and subject to fresh affordability and credit checks that you may not pass if your circumstances have changed.

To protect against offer expiry, consider the following strategies. First, choose a lender that offers extended mortgage offer validity for new build purchases — Barclays offers up to 12 months, while HSBC and NatWest offer up to 9 months. Second, time your mortgage application carefully: if the build is expected to take 10 months from the date you exchange contracts, applying too early means the offer may expire before completion. Third, maintain your financial profile throughout the build period: do not change jobs, take on new debt, or make other changes that could affect a re-application if the original offer expires.

The Complete Off-Plan Purchase Timeline

To bring all of these elements together, here is a typical timeline for an off-plan new build purchase from a major developer, showing the key milestones and financial events at each stage.

Snagging and Defects: Pre-Completion Checks

Before completion — or immediately after receiving access to the property — you have the right to carry out a snagging inspection to identify defects, incomplete work, or items that do not meet the specification agreed in your contract. While snagging is not directly related to the stage payment process, it is a critical step in the off-plan purchase that can identify issues before you take legal ownership.

Common snagging items in new build properties include paint defects (runs, drips, inconsistent coverage), poorly fitted doors or windows, scratched glass or surfaces, incomplete or damaged fixtures, uneven plastering, gaps in sealant around bathrooms and kitchens, external brickwork defects, and incomplete landscaping. Most developers will address genuine snagging items either before completion or within a reasonable period after you move in, typically under the terms of the NHBC or equivalent warranty.

Consider hiring a professional snagging inspector (typically £300 to £500 for a standard house) to carry out this check on your behalf. Professional snaggers know exactly what to look for and can identify issues that a layperson might miss. They will produce a detailed report listing all defects, which your solicitor can present to the developer before completion. Some issues may be significant enough to justify retaining a portion of the purchase price in escrow until they are resolved, though this is relatively unusual with major developers.

Financial Planning for Off-Plan Purchases

The extended timeline of an off-plan purchase requires more careful financial planning than a standard property purchase. Here is a comprehensive checklist of costs and considerations to factor into your budget.

One often-overlooked cost is the need to maintain your current living arrangements during the build period. If you are renting, you will continue paying rent until the new build is ready — and if the build overruns, this rent extends accordingly. Budget for at least 2 to 3 months more rent than the developer's estimated completion date suggests, as build overruns are very common. If you are selling an existing property to fund the new build, you will need to coordinate the sale with the new build completion, which adds another layer of complexity and potential cost if temporary accommodation is needed.

Final Thoughts: Managing the Off-Plan Journey

Buying a new build off-plan is an exciting process that allows you to secure a brand-new home, often at an advantageous price, and customise it to your preferences before construction is complete. However, the financial mechanics are more complex than a standard property purchase, and the longer timeline introduces risks and costs that require careful planning and management. Whether your purchase follows the standard completion model or involves CML stage payments, understanding the process ensures you are prepared for every eventuality.

The keys to a successful off-plan purchase are: choosing the right mortgage product with adequate offer validity (see our guide on how to compare mortgage deals for new builds), instructing a solicitor with specific new build experience, budgeting realistically for all costs including potential dual-payment periods, and maintaining close communication with the developer throughout the build. If you are considering an offset mortgage for your off-plan purchase, the build period can actually work in your favour, as your savings continue to offset the mortgage interest even before you move in. And if your credit history presents challenges, our guide on adverse credit mortgages for new build homes covers specialist options that may still make off-plan purchasing possible.